Business

US Job Growth Remains Modest as 2025 Draws to a Close

US job gains in December are expected to be modest, capping off one of the weakest years for employment growth since 2009. Economists anticipate that approximately 60,000 jobs were added for the month, according to the median forecast from a Bloomberg survey ahead of data release from the Bureau of Labor Statistics on January 5, 2026. This would bring total payroll additions for the year to around 670,000, a stark contrast to the 2 million jobs created in 2024.

The unemployment rate is projected to have eased to 4.5% in December, down from a four-year high. After years of intense competition for workers, employers have reduced hiring activity in 2025. The stabilization of job openings suggests that many companies are satisfied with their current staffing levels. Additionally, recent government trade-policy announcements have prompted firms to focus on cost-saving measures, leading to a more cautious approach to hiring.

Analysts note that the rapid adoption of artificial intelligence may also be contributing to limited payroll growth as companies seek to enhance productivity. Despite the slowdown in hiring, there are few indications of widespread layoffs, maintaining some stability in the job market. This situation is likely contributing to the Federal Reserve’s cautious stance regarding interest rate adjustments following three consecutive rate cuts at the end of 2025.

According to economists from Bloomberg Economics, “We think the decoupling between GDP growth and labor-market metrics will persist through 2026. Inflation will come down, and ultimately the Fed will cut rates by 100 basis points in the coming year.”

The upcoming jobs report for December will be accompanied by additional data from the Bureau of Labor Statistics, including figures for November regarding job openings, quitting rates, and layoffs. The Institute for Supply Management‘s December surveys of manufacturers and service providers will provide further insights into employment trends across those sectors.

As the week progresses, several important economic indicators will be released. The government will report on October housing starts, while the University of Michigan will issue its preliminary January consumer sentiment index. In Canada, job numbers are also expected, alongside inflation readings from Australia, the Eurozone, and Latin America.

In Europe, various reports will provide a clearer picture of inflation as the year concludes. Consumer-price figures from Germany and France for December will be released, followed by regional data the next day. The European Central Bank has indicated that inflation in the Eurozone is stabilizing at around 2%. Economists forecast that the headline inflation gauge will align with this target, while core inflation, which excludes volatile food and energy costs, may hold steady at 2.4%.

Other significant economic data will also be published, including manufacturing-related statistics from Germany, where factory orders for November are due. Industrial production data for Germany, France, and Spain will follow shortly thereafter. The deadline for applications for the second-highest position at the European Central Bank is approaching, as the finance ministers of the Eurozone prepare to select a successor for Luis de Guindos, whose term expires in May.

Inflation data from Switzerland is expected to show a slight increase, potentially reaching 0.1% in December, after an unexpected drop to zero in November. This aligns with the central bank’s forecast and would be significant, given that a negative reading would mark only the second occurrence of its kind in over four years.

In the UK, consumer lending numbers are anticipated to be a highlight, with no major data releases scheduled until the following week. Political discussions are expected to gain momentum as Parliament resumes following its recess.

In the Middle East, Turkish inflation data may indicate a slight slowdown to 31%, with Israel’s central bank likely to maintain current borrowing costs.

Across Asia, Australia’s consumer price index figures for November are due, with expectations that inflation has eased slightly but remains above the central bank’s target. This data will help the Reserve Bank of Australia assess recent price pressures. Japan’s wage growth is also anticipated to have slowed in November, though underlying momentum remains strong, supporting the Bank of Japan’s outlook.

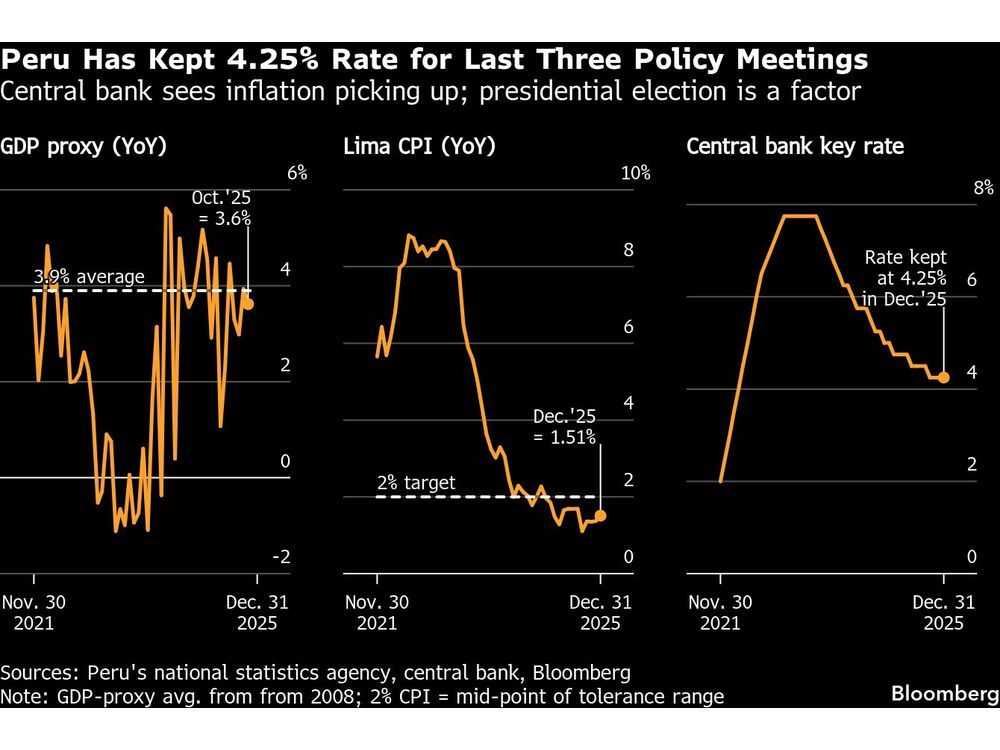

In Latin America, consumer prices will be central to economic discussions as major economies finalize their inflation data for 2025. Most analysts predict that inflation will return within central banks’ target ranges, with some adjustments to monetary policy expected in Chile, Peru, and Mexico.

As the global economy navigates these developments, cautious approaches from central banks will likely dominate discussions in early 2026.

Meta Plans Major Layoffs as AI Costs Surge

Alberta’s Referendum Could Pave Way for U.S. Statehood

Minooka District 201 Plans Enhanced Bilingual Support for Students

Canmore Approves Multiple Development Permits for New Projects

Remembering Bradly Castillo Shearsmith: A Life of Friendship and Joy

BIS Urges Watchdogs to Integrate Synthetic Risk Transfers in Stress Tests

Teva Transforms: Shifting Focus from Generics to Branded Success

Apple Launches AirPods Max 2 with Enhanced Audio Features

Ontario Ends Funding for Seven Supervised Injection Sites

Toyoake City Proposes Daily Two-Hour Smartphone Use Limit

Pedestrian Fatally Injured in Esquimalt Collision on August 14

B.C. Review Reveals Urgent Need for Rare-Disease Drug Reforms

Dark Adventure Game “Bye Sweet Carole” Set for October Release

Konami Revives Iconic Metal Gear Solid Delta Ahead of Release

Victoria’s Pop-Up Shop Shines Light on B.C.’s Wolf Cull

Jimmy Lai’s Defense Challenges Charges Under National Security Law

Snapmaker U1 Color 3D Printer Redefines Speed and Sustainability

Apple Expands Self-Service Repair Program to Canada

-

Science12 months ago

Science12 months agoToyoake City Proposes Daily Two-Hour Smartphone Use Limit

-

Top Stories12 months ago

Top Stories12 months agoPedestrian Fatally Injured in Esquimalt Collision on August 14

-

Health12 months ago

Health12 months agoB.C. Review Reveals Urgent Need for Rare-Disease Drug Reforms

-

Technology12 months ago

Technology12 months agoDark Adventure Game “Bye Sweet Carole” Set for October Release

-

Technology12 months ago

Technology12 months agoKonami Revives Iconic Metal Gear Solid Delta Ahead of Release

-

Lifestyle12 months ago

Lifestyle12 months agoVictoria’s Pop-Up Shop Shines Light on B.C.’s Wolf Cull

-

World12 months ago

World12 months agoJimmy Lai’s Defense Challenges Charges Under National Security Law

-

Technology12 months ago

Technology12 months agoSnapmaker U1 Color 3D Printer Redefines Speed and Sustainability

-

Technology12 months ago

Technology12 months agoApple Expands Self-Service Repair Program to Canada

-

Technology12 months ago

Technology12 months agoAION Folding Knife: Redefining EDC Design with Premium Materials

-

Technology12 months ago

Technology12 months agoSolve Today’s Wordle Challenge: Hints and Answer for August 19

-

Business12 months ago

Business12 months agoGordon Murray Automotive Unveils S1 LM and Le Mans GTR at Monterey